What Is a CD Account?

Everything You Need to Know

A CD account (Certificate of Deposit) is a federally insured savings product offered by banks and credit unions that pays a fixed, guaranteed interest rate in exchange for keeping your money deposited for a set period — typically ranging from 3 months to 5 years. At maturity, you receive your principal plus all earned interest. CDs consistently offer higher rates than standard savings accounts, making them one of the safest, most predictable wealth-building tools available to American savers.

What Is a CD Account?

A CD account, short for Certificate of Deposit, is a time-based savings deposit offered by banks, credit unions, and some online financial institutions. Unlike a regular savings account where you can deposit and withdraw money freely, a CD requires you to lock in a specific amount of money for a defined term — and in return, the institution guarantees a fixed interest rate higher than most other deposit products.

Think of a CD as a deal between you and your bank: you promise to leave a set amount of money untouched for a fixed period, and the bank promises to pay you a higher, locked-in interest rate for the privilege of using those funds. It’s one of the oldest, most trusted financial products in American banking — and in today’s elevated-rate environment, one of the most rewarding low-risk options available.

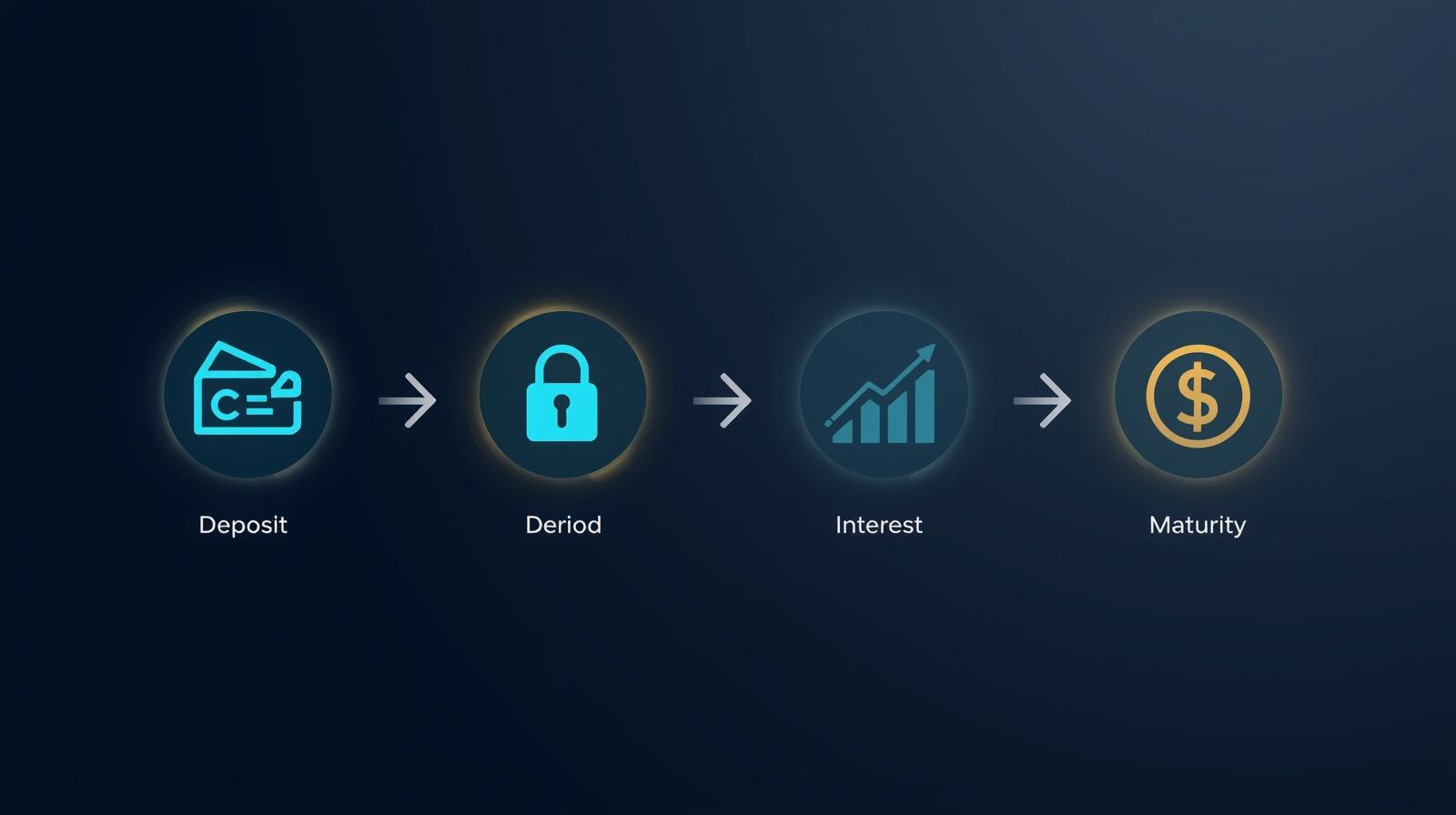

How Does a CD Account Work?

Opening and operating a CD account is straightforward. Here is the complete lifecycle of a typical CD, from opening day to maturity — so you know exactly what to expect at every stage.

-

01

Choose Your Term and Deposit Amount

Select a term (e.g., 6 months, 1 year, 3 years) and decide how much to deposit. Most banks require a minimum of $500–$1,000; many online banks have no minimum.

-

02

Lock In Your Interest Rate

The bank confirms your APY on the day you open the CD. This rate is guaranteed for the entire term — even if market rates drop significantly afterward.

-

03

Interest Compounds Over Time

Your interest compounds monthly or daily (depending on the bank) and is added to your balance, accelerating growth through the power of compound interest.

-

04

CD Reaches Maturity

At the end of the term, the CD “matures.” You receive your full principal plus all earned interest. Most banks give you a 7–10 day grace period to decide what to do next.

-

05

Reinvest, Withdraw, or Roll Over

You can withdraw your funds, open a new CD at current rates, or let the bank automatically roll it over into a new CD term (often at a lower default rate — so always review before auto-renewal).

Grace Period: Federal regulations require most banks to provide a minimum 7-day grace period after maturity. Use this window to shop rates before your CD auto-renews into a potentially lower-rate product.

Types of CD Accounts

Not all CDs are created equal. American banks and credit unions offer several varieties of CD accounts, each designed to address different savings goals, risk tolerances, and market conditions.

Traditional CD

The standard CD — fixed rate, fixed term, fixed deposit. You commit a lump sum for a defined period and earn a guaranteed rate. Early withdrawal triggers a penalty. Best for savers who are certain they won’t need the funds before maturity.

No-Penalty CD (Liquid CD)

Allows you to withdraw funds before maturity without facing an early withdrawal penalty. Rates are typically slightly lower than traditional CDs, but the flexibility can be worth it — especially for emergency fund allocation.

Bump-Up CD

Lets you request a one-time rate increase if your bank raises its CD rates during your term. Useful in a rising-rate environment, though the starting rate is usually slightly below standard CD rates.

Step-Up CD

Automatically increases your rate at set intervals throughout the term — for example, every 6 months. Provides built-in rate growth without requiring action on your part.

Jumbo CD

Requires a minimum deposit of $100,000 or more. Jumbo CDs may offer slightly higher rates than standard CDs, though the gap has narrowed at many institutions. FDIC insurance still applies up to $250,000.

IRA CD

A CD held inside an Individual Retirement Account (Traditional or Roth IRA). Combines the guaranteed returns of a CD with the tax advantages of an IRA. Ideal for near-retirees who want capital preservation within their retirement portfolio.

| CD Type | Early Withdrawal | Rate Flexibility | Best For |

|---|---|---|---|

| Traditional CD | Penalty applies | Fixed | Certain time horizons |

| No-Penalty CD | No penalty | Fixed (lower) | Emergency funds |

| Bump-Up CD | Penalty applies | One-time bump | Rising rate outlook |

| Step-Up CD | Penalty applies | Auto-increases | Long-term savers |

| Jumbo CD | Penalty applies | Fixed (premium) | Large deposit holders |

| IRA CD | IRA rules apply | Fixed | Retirement savers |

CD Interest Rates & How They’re Calculated

CD interest rates are driven primarily by the Federal Reserve’s federal funds rate. When the Fed raises rates, CD yields follow. When the Fed cuts rates, new CD offers become less attractive — which is why locking in a competitive rate during a high-rate period is such a valuable move for savers.

CD interest is calculated using the compound interest formula, which accounts not just for interest on your original deposit, but also for interest earned on previously accumulated interest:

P = Principal (initial deposit)

r = Annual interest rate as decimal (5% = 0.05)

n = Compounding periods per year (12 = monthly)

t = Term in years

Real Example: $10,000 CD at 5% APY for 3 Years

The APY (Annual Percentage Yield) is the most important number to compare between banks. Unlike APR, APY factors in compounding and gives you the true annualized return. Federal law (Truth in Savings Act) requires all US banks to disclose APY — so always use this figure when evaluating competing CD offers.

Pros and Cons of CD Accounts

Like any financial product, CDs have clear strengths and genuine limitations. Understanding both helps you determine whether a CD fits your specific financial situation.

- Guaranteed, fixed interest rate — immune to market volatility

- FDIC or NCUA insured up to $250,000

- Higher yields than regular savings or checking accounts

- Predictable, projectable returns — easy to plan around

- Wide range of term options from 3 months to 5+ years

- Available at virtually every US bank and credit union

- Encourages disciplined saving by locking in funds

- Early withdrawal penalties can erase interest earned

- No flexibility to add funds after opening (standard CDs)

- Returns don’t keep pace with stock market in bull markets

- Interest taxed as ordinary income each year

- Inflation risk on long-term CDs if rates rise sharply

- Opportunity cost if rates climb significantly post-lock-in

Bottom Line on Risk: For money you can afford to leave untouched, CDs are among the lowest-risk financial instruments available in the United States. The key is matching the CD term to your actual financial timeline so you never need to trigger a penalty.

CD Account vs Savings Account vs Money Market

Many American savers wonder how CDs compare to high-yield savings accounts and money market accounts. Each serves a different purpose, and the best choice depends on your liquidity needs and time horizon.

| Feature | CD Account | HYSA | Money Market |

|---|---|---|---|

| Interest Rate | Highest (fixed) | High (variable) | High (variable) |

| Liquidity | Low (locked term) | Full access | Full access |

| FDIC Insured | Yes ($250K) | Yes ($250K) | Yes ($250K) |

| Rate Changes | Fixed at opening | Can drop anytime | Can drop anytime |

| Min. Deposit | $0–$1,000+ | $0–$100 | $0–$2,500 |

| Best For | Defined time horizon | Emergency fund | Active cash management |

The defining advantage of a CD over a high-yield savings account is rate certainty. A HYSA’s rate can be cut at any time — and frequently is when the Fed lowers rates. A CD locks in your rate the day you open it, protecting you from rate cuts for the entire term. This makes CDs particularly valuable in a rate-declining environment.

Don’t Over-Commit: Never put money into a CD that you might need before maturity. Keep 3–6 months of living expenses in a liquid savings account, then invest additional savings in CDs for higher, protected yields.

How to Open a CD Account

Opening a CD is one of the simplest financial transactions you can make. Most US banks allow you to open a CD entirely online in under 10 minutes. Here’s exactly what the process looks like.

-

01

Compare Rates Across Institutions

Check online banks (often highest rates), credit unions, and traditional banks. Focus on APY — not APR — for accurate comparisons. Rate aggregator sites like Bankrate and NerdWallet are useful starting points.

-

02

Confirm FDIC or NCUA Insurance

Verify the institution is FDIC-insured (banks) or NCUA-insured (credit unions). Never deposit in an uninsured institution, regardless of the rate offered.

-

03

Gather Your Documents

You’ll need your Social Security Number, a government-issued photo ID, and your bank account details (routing and account number) for the initial funding transfer.

-

04

Choose Your Term and Open Online

Select the term that aligns with your financial goals. Complete the online application, fund the account via ACH transfer, and your CD is open. You’ll receive a confirmation with your exact maturity date and APY.

-

05

Set a Maturity Reminder

Mark your calendar 2 weeks before maturity. This gives you time to shop rates and decide whether to withdraw, reinvest, or roll over — rather than defaulting into the bank’s standard renewal rate.

Expert Tips to Maximize Your CD Account

Simply opening a CD is a good move. Opening the right CD at the right time with the right strategy is a great move. These field-tested approaches are used by financially savvy Americans to extract maximum value from their fixed-income savings.

Build a CD Ladder

Rather than committing all your savings to one long-term CD, spread your money across multiple CDs with staggered maturity dates — 1-year, 2-year, 3-year, 4-year, and 5-year. As each rung matures, you reinvest at the best available rate. This strategy delivers higher average yields than short-term CDs while ensuring a portion of your money becomes accessible each year.

Prioritize Online Banks

Online-only banks consistently offer CD rates that are 0.5% to 1.5% higher than traditional brick-and-mortar institutions. Because they operate without the overhead of physical branches, they pass the savings to depositors through better rates. All major online banks are FDIC-insured, making them just as safe as your local bank.

Leverage IRA CDs for Tax Efficiency

CD interest is taxed as ordinary income. Holding your CDs inside a Traditional or Roth IRA eliminates annual tax drag — either deferring taxes until retirement (Traditional) or eliminating them entirely on qualified withdrawals (Roth). For high-income savers, this can meaningfully boost after-tax returns.

Watch for Promotional CD Offers

Banks frequently launch promotional CDs at unusual terms — 7-month, 11-month, 15-month — with rates above their standard offerings. These “specials” can be highly lucrative. Monitor your bank’s rate page regularly or sign up for rate alerts.

Pro Move: When a CD matures, don’t just auto-renew. Take the grace period to compare rates from at least 3 institutions before committing. A 0.5% rate difference on $50,000 over 3 years equals over $750 in additional earnings.

Frequently Asked Questions

Real answers to the most common questions US savers ask about CD accounts.

Yes — especially for savers who have a defined time horizon and want guaranteed returns without market risk. In 2026, many online banks still offer competitive CD rates well above what standard savings accounts provide. For any money you don’t need immediate access to, a CD locks in a premium rate and protects you from future rate cuts.

If your bank is FDIC-insured (and virtually all US banks are), your deposits — including CDs — are protected up to $250,000 per depositor, per institution. If the bank fails, the FDIC steps in and either transfers your CD to another institution or pays you the full principal plus accrued interest. You will not lose money.

At an FDIC-insured bank, you cannot lose your principal in a CD. The only way to lose money is if you withdraw early and the early withdrawal penalty exceeds the interest earned — but even then, the worst case is a small reduction in interest, not a loss of principal. CDs are one of the safest savings instruments in the US financial system.

It depends on your principal, APY, compounding frequency, and term. For example: $10,000 at 5% APY compounded monthly for 3 years earns $1,614.72 in interest (total balance: $11,614.72). Use a CD calculator like cdcalculatorpro.us to get exact projections for your specific scenario instantly.

It varies by institution. Many online banks have no minimum deposit requirement. Traditional banks typically require $500–$2,500. “Jumbo CDs” — which may offer slightly higher rates — require $100,000 or more. Some of the highest-yielding CDs in the market are available with no minimum deposit from online institutions.

Yes. The IRS treats CD interest as ordinary income, taxed at your marginal federal income tax rate. You’ll receive a Form 1099-INT from your bank each January covering interest credited in the prior year — even on multi-year CDs where you haven’t yet withdrawn the funds. Holding CDs inside an IRA eliminates or defers this tax burden.

An early withdrawal penalty (EWP) is a fee charged when you access your CD funds before the maturity date. Penalties are typically expressed as a number of months’ worth of interest — for example, 3 months’ interest for a 1-year CD, or 12 months’ interest for a 5-year CD. In rare cases (very early withdrawal from a long-term CD), the penalty could reduce your principal. Always review EWP terms before opening.

The primary differences are rate and liquidity. A CD offers a higher, fixed rate but locks your money in for a set term with an early withdrawal penalty. A savings account offers lower, variable rates but allows deposits and withdrawals at any time. CDs are best for money with a defined future purpose; savings accounts are best for emergency funds and ongoing cash management.

Our Other Calculators & Tools

Ready to Put Your Savings to Work?

A CD account is one of the simplest, safest, and most rewarding tools in the American saver’s toolkit. Whether you’re parking an emergency fund in a no-penalty CD, building a ladder for predictable returns, or locking in today’s elevated rates before they drop — there’s a CD strategy that fits your goals. Use our free CD calculator to project your exact returns before you commit.